Disclaimer and Acknowledgements: This blog post has been reproduced, with thanks, from The Financial Post’s Haider-Moranis Bulletin, courtesy of Murtaza Haider and Stephen Moranis, published on April 25, 2019.

Conventional wisdom states that falling prices should improve housing affordability.

Though the logic is appealing, Canadian housing markets paint quite a different picture, with housing affordability worsening even though average housing prices have fallen.

Unlike many other assets classes, housing markets are complex and heterogeneous, with no two homes (or buyers) being identical. As a result, the housing market does not necessarily follow the typical wisdom of markets.

Recent housing market data and research reveal that affordability eroded in Canada even as prices have tumbled. The reason for this anomaly is that housing affordability only partially depends on prices. Regulatory changes also play a large role in determining housing affordability.

A report by RBC Economic Research reviewed housing affordability in the third quarter of 2018 and concluded that it was “getting less affordable to own a home in Canada.”

The report tracks the income required to cover the cost of owning an average home with a 25 per cent down payment. When compared with the third quarter of 2015, the qualifying income had increased significantly by the third quarter of 2018.

In Vancouver, for instance, the income required to cover ownership of an average home was $211,000 in 2018, up from $127,000 three years ago. The qualifying income in Toronto was $187,000 in 2018 compared to $103,000 in 2015. In fact, the qualifying income had increased in all large and small housing markets across Canada.

One big reason for the higher qualifying income required in 2018 was the increase in housing prices since 2015, a rise that was most pronounced in Greater Vancouver and Toronto.

Qualifying incomes, therefore, increased by $34,000 in Vancouver and $27,000 in Toronto since 2015 as a result of higher prices, the RBC report estimated.

But rising prices were not the only factor. Even without their impact, the qualifying income would have climbed considerably because of the stress test that required the borrowers to qualify at a higher interest rate than the contracted rate as of January 2018.

The RBC report estimated that the increase in qualifying income due to the stress test was almost the same as the one resulting from the increase in housing prices.

The stress test raised the qualifying income threshold by $36,000 in Vancouver and $27,000 in Toronto.

Recent housing market data and research reveal that affordability eroded in Canada even as prices have tumbled. Tyler Anderson/National Post files

It also didn’t help that mortgage rates also increased over the same period further raising the bar to qualify for home ownership.

The RBC Economics Report illustrates the peculiarities of housing markets where price alone does not determine the affordability of an asset. Certainly, the increase in housing prices eroded affordability. However, equally instrumental were the regulatory changes (stress test and mortgage rates) that also erected huge affordability barriers.

The impact of the stress test is further illustrated with data from Toronto where housing prices rose sharply from 2015 to the first quarter of 2017. Toronto’s housing market experienced two regulatory shocks. The first shock came in April 2017 when the Ontario government imposed new taxes on foreign homebuyers. The immediate impact was a decline in sales and prices. The second shock came in January 2018 when the stress test was imposed.

Toronto’s sales data reveals that the share of the market taken up by the least expensive homes (those sold for less than $400,000) declined as housing prices increased.

For instance, 30 per cent of the homes sold in 2015 transacted for less than $400,000. By the first quarter of 2017, when housing prices peaked, the share of low-priced homes accounted for a mere 12 per cent of the transactions.

As the housing prices slid in Toronto as of May 2017, the share of homes that transacted for less than $400,000 increased slightly and represented 13 per cent of the total transactions for the rest of 2017.

However, the share of low-priced homes in 2018 declined from 13 to 9 per cent (a 31 per cent drop), which took place even when the nominal average home price in Toronto declined from $822,681 in 2017 to $787,300 in 2018, and $766,197 in February 2019.

Again, the conventional wisdom would have dictated an increase rather than a decline in the share of low-priced homes that attract low- to moderate-income households. But that didn’t happen.

The stress test and the increase in mortgage rates increasingly affected the affordability of low-income households and priced them out of the market even when house prices were declining.

Housing affordability will improve with a decline in home ownership costs, which will require regulatory changes in the short run and greater housing supply in the long run.

Disclaimer and Acknowledgements: This blog post has been reproduced, with thanks, from The Financial Post’s Haider-Moranis Bulletin, courtesy of Murtaza Haider and Stephen Moranis, published on March 13, 2019.

Murtaza Haider is an associate professor at Ryerson University. Stephen Moranis is a real estate industry veteran. They can be reached at www.hmbulletin.com.

]]>CIBC says drop in big-city mortgage markets has been larger and longer than expected

A surprise jump in housing sales in greater Toronto in April is being interpreted in some quarters as a sign of a spring recovery in the housing market.

But market movements in other parts of the country have been much more nuanced, making any broad statement about a sustainable recovery impossible at this point.

The April figures were dominated by a spike in Toronto where sales increased from 7,159 units in March to 9,042 units. The average (nominal) housing price there also increased to $820,148. The last time average price crossed the $800,000 mark was in October 2018.

While the improved conditions were welcomed by most, the question of why sales and prices jumped — and whether those gains will continue through the summer — is still in need of an answer.

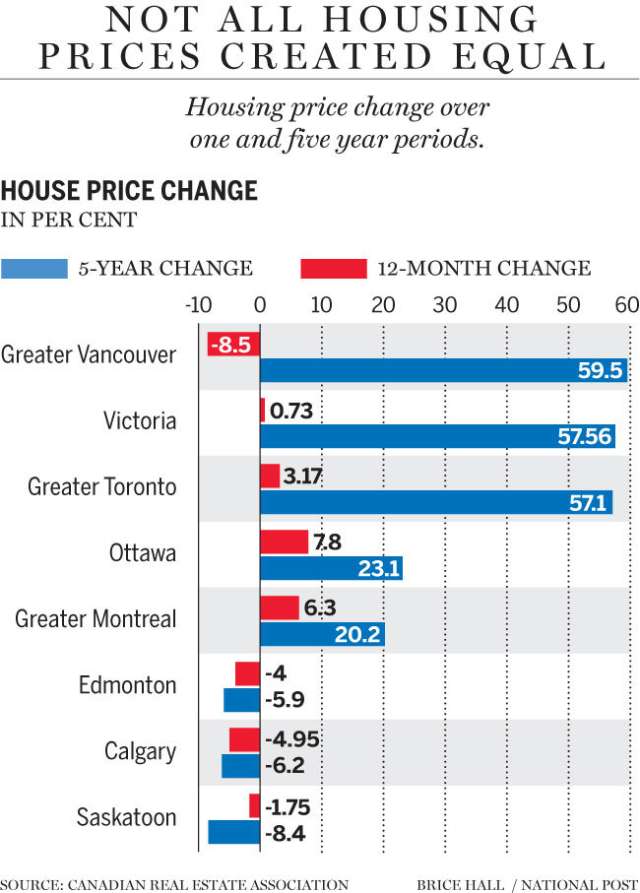

By contrast, sales continue to struggle in B.C. and prices in the urban housing markets in Alberta and Saskatchewan are now lower than they were five years ago.

Housing markets in B.C. are still moderating from stringent regulations imposed by the provincial and federal governments. Year-over-year sales in Vancouver were down by almost 30 percent in April. Residential sales in the Fraser Valley and Victoria, the other large housing markets in the province, were down by 19 and 10 percent respectively.

The MLS Composite Home Price Index (HPI) Benchmark Price, which takes into account size and structure type, reported year-over-year declines for greater Vancouver and neighbouring housing markets. HPI reported a modest year-over-year increase in Victoria.

Housing sales in markets immediately east of B.C. were higher. Calgary and Edmonton reported modest year-over-year increases whereas sales jumped by 28 and 18 per cent in Regina and Saskatoon respectively. However, the smaller size of the prairie market means that it would only take a few hundred additional sales to significantly move the needle.

Despite the increase in sales, prices are declining in Alberta and Saskatchewan. Though the magnitude of the decline in prices is lower in comparison to the ones observed in B.C., the falling housing prices have lasted much longer in the prairies than elsewhere.

Consider that housing prices in B.C., despite the recent declines, are still 60 to 80 per cent higher than they were five years ago. It’s not the same for the markets in Alberta and Saskatchewan where prices in April were lower than the prices five years ago.

Housing markets in Ottawa and Montreal are distinct from other large cities. Not only have they reported modest year-over-year increases in April —7.7 and 6.3 per cent in Ottawa and greater Montreal respectively — prices have increased moderately over the five-year horizon. The HPI in April was 23 and 20 per cent higher over five years in the two cities.

Compared to the markets in Toronto and Vancouver, Ottawa and Montreal have avoided rapid price inflations that raised alarms about housing affordability. A substantial cohort of renters, which dominates the housing market in Montreal, has likely contributed to a modest increase in demand for owner-occupied housing resulting in a moderate increase in housing prices.

By comparison, Ottawa is likely to have benefitted from the large number of federal government employees who constitute a big part of the regional labour force and whose numbers and incomes are more stable, which prevents rapid demand shocks.

Across Canada, housing sales in April were up by 4.2 per cent year-over-year. The national HPI though faltered slightly by 0.3 per cent. Higher sales in April 2019 relative to the same month last year are encouraging, but come off a relatively low reference point: sales in April 2018 were the lowest for an April in the past seven years.

The diverse spectrum of housing outcomes in large cities indicates that local housing markets are not on the same cycle. While some markets might have started to recover, others still have to experience additional moderation in sales and prices.

While it is tempting to have a one size fits all policy response to housing market challenges, one runs the risk of compounding the problems for markets needing a custom response.

Tailoring regulatory interventions to address local market needs would be a better approach.

Disclaimer and Acknowledgements: This blog post has been reproduced, with thanks, from The Financial Post’s Haider-Moranis Bulletin, courtesy of Murtaza Haider and Stephen Moranis, published on May 23, 2019.

Murtaza Haider is an associate professor at Ryerson University. Stephen Moranis is a real estate industry veteran. They can be reached at www.hmbulletin.com.

]]>

One in three Canadian households lives in a rental unit. In populous municipalities, the fraction increases to one in two.

Yet rental housing remains a sidebar in the housing narrative, which focuses overwhelmingly on home prices and mortgage rates. As homeownership continues to slip out of the hands of younger cohorts due to rising prices, renting remains the only viable alternative.

Households facing affordability challenges have consequently lengthened their rental tenures resulting in very low rental vacancy rates and rapidly rising rents. In Vancouver, Canada’s third-largest residential rental market, vacancy rates in October 2018 averaged around one percent, whereas the increase in average rents equaled 6.8 percent year-over-year (YOY).

The rental situation was not much different in Toronto. However, in Montreal, Canada’s largest residential rental market, vacancy rates in October 2018 declined by 33 percent accompanied by a four percent increase in average rents (YOY).

Low vacancy rates and rising rents define the rental housing markets in large cities across Canada. The average rent for a two-bedroom unit in October last year was $1,467 in Toronto and $1,649 in Vancouver. While vacancy rates are higher in Calgary and Edmonton than in Toronto and Vancouver, Alberta is nevertheless seeing a trend toward lower vacancy rates and higher rents.

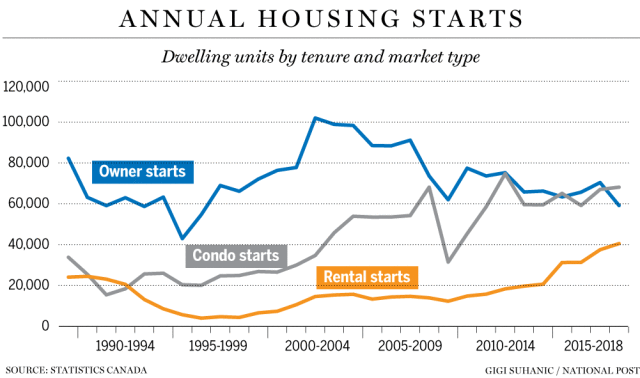

Insufficient rental housing supply seems to be the culprit. Many industry observers cite a four-decade-long drought in the supply of new purpose-built rental units. The investment in condominiums over the years, of which many units are acquired as an investment and rented out subsequently, to an extent compensated for lack of investment in purpose-built rentals.

However, purpose-built rentals offer tenure security that is missing in rented condominiums where a landlord can, at their discretion, withdraw the unit from the rental market.

Rental properties in Calgary. Jeff McIntosh/The Canadian Press

Housing experts believe that the supply of rental units dried up in the seventies because of two changes in public policy. First, oft-cited rent control (vacancy decontrol) regulations by various provincial governments, introduced initially in the early seventies, is believed to have dissuaded investors from rental markets.

The second public policy change involved the federal government introducing the capital gains tax, which was also applied to purpose-built rental properties. And since the tax is applied to nominal values, a landlord is expected to pay taxes on nominal and not a real increase in property values. In times of high inflation, the tax will have a significant adverse impact on profitability.

The Canadian Federation of Apartment Associations, an industry group representing the private residential landlords who own or manage approximately one million rental units, have put these concerns on the agenda for their next annual meeting to be held in May in Toronto.

John Dickie, the Federation’s president, believes that all tiers of government have to make changes to ensure renting is a healthy and a viable housing alternative for Canadians. He believes that the feds must reform the tax policy for rental buildings so that the capital gains tax does not continue to be a deterrent for investment in rental housing.

“The provinces and cities need to look hard at development charges, delays in planning approvals, and rent control restrictions. Those are the most important factors holding back much-needed purpose-built rental supply,” Dickie said.

There is some good news on the rental front. The past few years have seen the beginnings of a resurgence in rental housing construction. Starts have accelerated to the extent that in 2018 rental starts were twice the number recorded in 2014.

Low rental vacancy rates and rising rents in the recent past have started to attract new investment in rental housing construction. However, waiting for rents to rise to send a signal to investors might not be the best public policy.

Higher rents disproportionately affect housing affordability for those who struggle with securing adequate shelter for their families.

Thus, a preferred public policy response for affordable rental housing should not be a reliance on the market forces that will require the rents to rise before investment pours in.

Instead, public policy interventions, such as reviewing capital gains for rental housing, streamlined municipal approval processes and eliminating rent control regulations that discourage new rental construction can help ensure a steady and sufficient rental supply for a balanced housing market in Canada.

Murtaza Haider is an associate professor at Ryerson University. Stephen Moranis is a real estate industry veteran. They can be reached at www.hmbulletin.com.

]]>